More FI’s onboard customers and operate digitally than they have ever done before, this digital adoption is only going to accelerate as more people expect more personalized, transparent and interconnected services from their financial institutions. We anticipate at Lynx that several players will operate in the intersection of finance and social, likely these players will enable embedded finance and push forwards instant realtime seamless financial experiences through super apps.

Articles

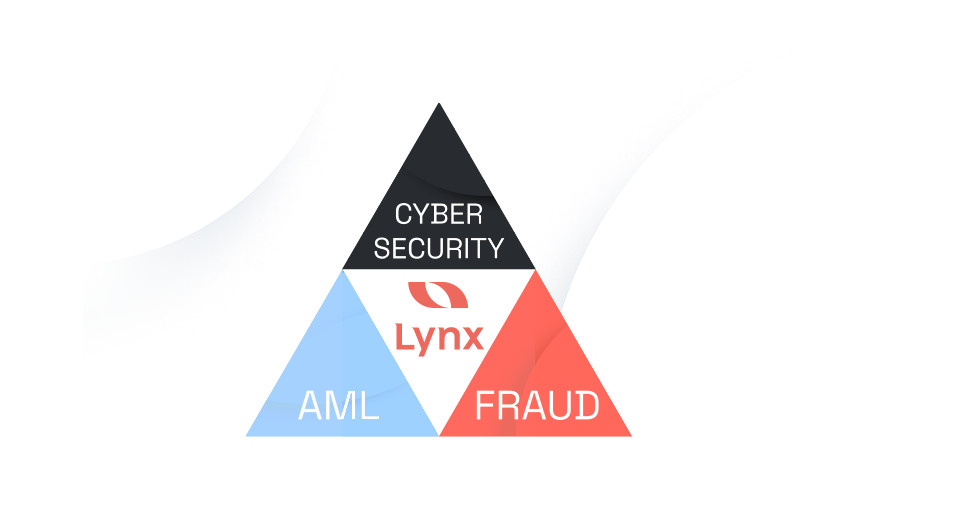

Triforce: The convergence of Fraud, AML and Cyber Security

25 Sep 2023

Share

The past

It has long been the case that Fraud Prevention, Anti Money Laundering and Cybersecurity are separate solutions with their own specific use cases that they address.

Fraud Prevention has somewhat sat between the two trying to take the best from both sides, but if you’re a financial institution it was expected that you would buy an isolated solution to address AML, an isolated solution to address Fraud, and an isolated solution to address Cybersecurity.

Triforce: Fraud Prevention, Anti Money Laundering and Cybersecurity

It makes sense when you consider how Financial Institutions organically added to their products. In that they specifically offered solutions by channel without consideration of interoperability or the unification of the technology stack and the risk tools sitting on that level. Simply due to the maturity of difital banking and the understanding of the interconnectedness of user journeys and data.

What this can result in:

- Each channel has its own point solution

- The solutions do not talk to one another

- There is no sharing of intelligence

- Each solution does something different in a unique way

- There is a need to connect the solutions with a middleware

- The FI’s have to deploy a team to each solution

- Attackers just have to find the weakest solution in the financial institution to be successful

- There is increased operational cost

- There is increased fraud

But all that’s about to change.

The Future

More FI’s onboard customers and operate digitally than they have ever done before, this digital adoption is only going to accelerate as more people expect more personalized, transparent and interconnected services from their financial institutions.

We anticipate at Lynx that several players will operate in the intersection of finance and social, likely these players will enable embedded finance and push forwards instant realtime seamless financial experiences through super apps.

Just as financial institutions are going through their biggest changes yet through digital transformation they expect their technology stack to progress with them and the vendors they use to follow suit. We’re here to tell you many can’t, but we at Lynx have the vision and agility to do so.

Datos Insights agree, and recently wrote a report based on the current state of Fraud and AML Machine Learning Platforms.

The key take away from the report:

- Fraud and AML Market synonymous with FI Products / Channels

- Market value 2019 $1bn, projected to increase to $7bn 2024 EoY

- FI Drivers:

- Optimize balance between loss reduction,

- Operational efficiency,

- Regulatory compliance

- And seamless client experiences

- FI’s looking to consolidate ML platforms across Fraud and AML business units

- Most FI’s very early in journey toward authoring and deploying own ML models

- Overall cost for new / upgraded technology, finding necessary budget and resourcing, can present substantial hurdles to adoption

- Best in class solutions scored high

- ML product suites, model development, performance, governance

- Service and support capabilities[1]

The Present

What does a next generation Fraud Prevention and AML ML solution look like and who will own it?

It is perhaps easier to answer the second part of the question first, likely this will be owned by the cyber fusion centre.

There is an additional transformation happening within financial institutions, mainly the cyber fusion centre. This is the coming together under the cyber security division of fraud, AML, and cyber security tools to increase:

- Technical Threat Intelligence

- Strategic Theat Intelligence

- Threat Response

- Security Orchestration, Automation, and Response (SOAR)

As to what will the solution look like. We expect that it will evolve AML digitally, bring fraud prevention forwards in terms of machine learning and forensics with overarching key components shared across the tools. These are:

- Interfaces

- Enrichment

- Feature / Variables

- Machine Learning Models

- Decision Engine

- Workflows / Orchestration

- Responses

- Investigation / Forensics

- Intelligence Network

Why it matters

Attackers have identified that they can scale up their operations by using the digital channels, automation and AI against the FI.

The attacker is able to harvest, purchase, generate real and or synthetic identities on mass and automate their attack with the financial institution.

The impact is that data that was used historically to go through KYC and due diligence doesn’t have the same level of surety and human belonging as it’s fake or stolen. As such onboarding has to evolve to make use of digital data that Fraud Prevention and Cyber Security teams have used for some time.

For example, you can identify the device, location, user agent and cookies of the application to understand if they are part of a compromised list of attribute associated to an organised crime group trying to build a network of mule accounts in your financial institution.

Or you can make use of intelligence networks to identify deliberately obfuscated links between criminals and the applicant.

A big problem for both Fraud and AML is that analysts are inundated with alerts based on rule matches. By using highly effective machine learning (ML) models you can reduce the amount of false alerts by up to a factor of 10 compared to other ML solutions using unsupervised learning. The implementation of supervised machine learning improves the accuracy of the rules using a risk score. Thus reducing the amount of people needed, and improving the time the analysts spend investigating.

Another problem is the capability to get a holistic view of the user and their associated entities, this can be solved with combined advanced entity link analysis tools. Thus enabling analysts to come to quicker decisions on alerts and find connected undetected criminal networks.

The future problem will not be know your customer or know your business, instead it will be know your identity and aversaries will continue to innovate thus obfuscating and adding layers to the identity they pose to be.

Solutions best prepared to seamlessly work with embedded finance, digital identity, intelligence networks and were born out of machine learning will outperform legacy point solutions.

That’s why we at Lynx are forging a path for our solutions to digitally enrich and converge changing the narrative from know your customer to know your identity.

Why not find out more and watch us as we evolve to bring fraud, aml and cybersecurity together and a next generation identity.

[1] https://aite-novarica.com/report/aite-matrix-leading-fraud-aml-machine-learning-platforms

Copied link